VIX Futures — an Overview with 4 Basic Trading Strategies

This is the 3rd story our “Journey to Vol Trading” series that chronicles the evolution of our trading. Keep reading for updates.

As we continued our journey in volatility trading, it became clear that VIX Futures would be the best way to take positions on long or short volatility predictions. We reviewed the basics of VIX Futures in the previous article, and now we will take a deeper dive into their unique characteristics.

Contango and Backwardation

The critical feature of VIX futures is how each future month’s price relates to the current value of the VIX Index itself.

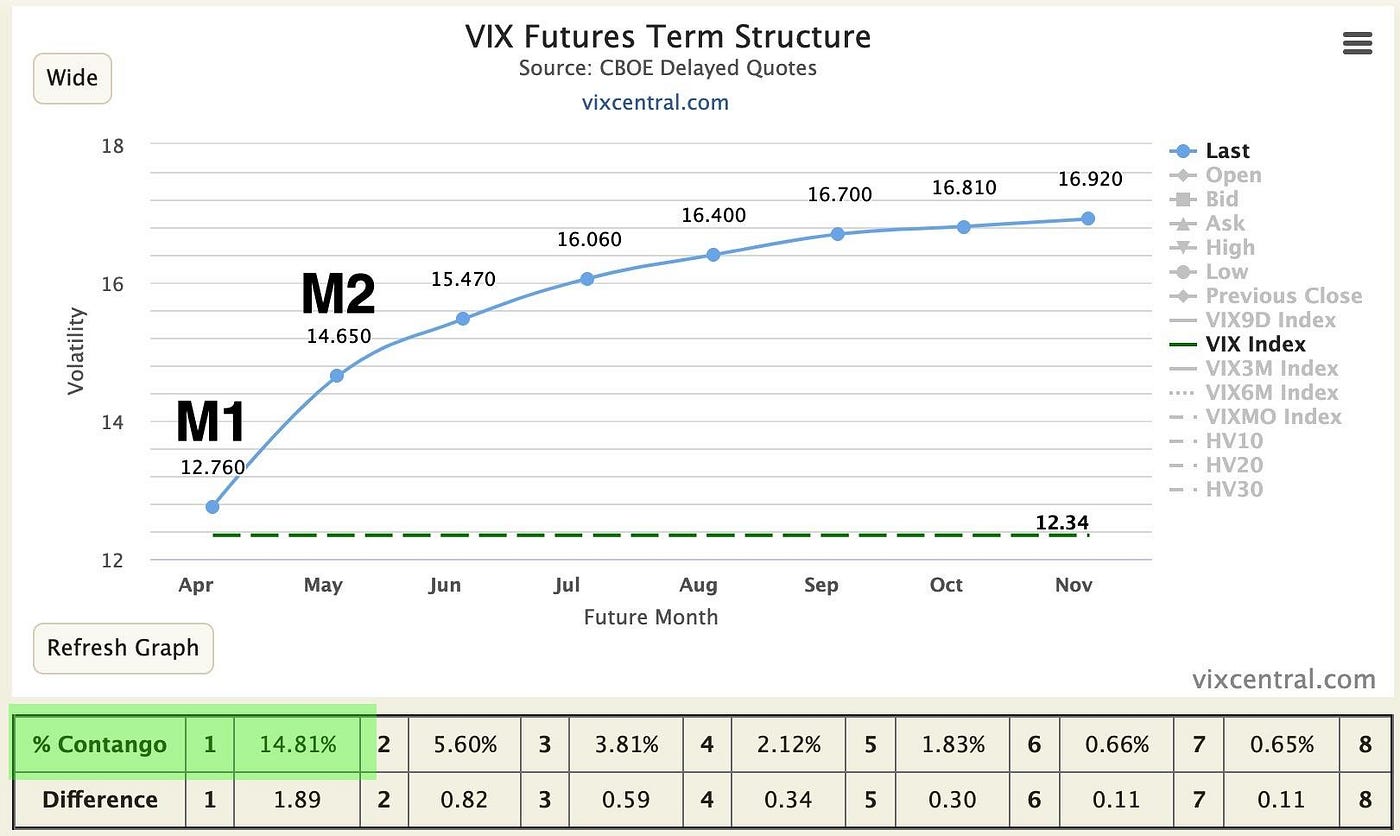

When futures are priced above the current VIX Index, the VIX Futures Term Structure is known as being in Contango.

Most commodities like energy (Oil, Gas) or food (Soybeans, Corn) are almost always in Contango due to the cost of storage. In simple terms, if a barrel of oil is worth $50 today, and it costs $1 per month to store it, then a Futures contract with delivery in 1 month would be $51, while a contract with delivery in 2 months would be $52 etc. Food and most other physical commodities follow the same concept.

Since the VIX is an index, and the futures are cash settled, it seems initially strange that VIX Futures would be in contango since there is no cost of storage. In this case, contango derives from the market’s general anticipation that the VIX will rise in the future. Many traders use VIX Futures as protection, similar to how they would use S&P 500 Put options. They purchase VIX Futures so that if the market turns south, and the VIX goes up (as it usually does in that case), they will offset their losses in stocks with gains in the VIX futures.

Just like options have a premium, VIX futures usually have a premium as well, which is known as Volatility Risk Premium (VRP) and is the cost that investors are willing to pay to insure their portfolios against the increase in volatility.

Since the S&P 500 spends about 80% of the time in an uptrend, which leads to a low VIX, its Futures are usually in Contango because investors are protecting against an eventual increase in the VIX. We will talk about the trading opportunity that consistently occurs as a result of this phenomenon shortly. But first, let’s talk about Backwardation

When VIX Futures are lower than the current VIX Index, the futures are set to be in Backwardation. This happens much more rarely than Contango.

The concept of Backwardation centers around the idea that the future value of an item is less than it is currently. The easiest way to understand that is stocks with dividends. The S&P 500 index is a group of stocks that pay a quarterly dividend, so that the longer you hold it, without any change in the actual price of the stocks, the more money you make. In the case of S&P 500 futures, the delivery of the actual stocks in say 6 months from now should be worth less than the current price of the stocks because the seller of the future (the one who currently holds the stocks and will deliver them in 6 months) will collect the dividends in the meantime. In practice, interest rates on cash of course affect the price of futures also (since the buyer of the future gets to hold on to the cash and receive interest until they have to buy the stocks in 6 months). Therefore, S&P 500 futures are generally in backwardation when the dividends of the S&P 500 are higher than the risk free interest rate available on cash.

When it comes to VIX Futures, the main driver of backwardation is simply expectations of future volatility. As we discussed earlier, the VIX is mean reverting, such that spikes tend to be followed by periods of lower volatility and lower VIX. When the VIX spikes, investors who were using VIX futures to hedge their portfolio realize their gains, and the remaining speculators anticipate that the VIX will fall (which it always does, over an extended enough period of time).

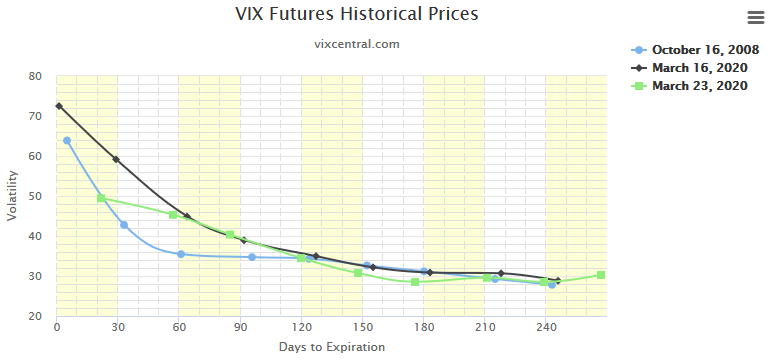

On dates where the market fell and the VIX spikes significantly above its historical average range (which is typically between10 to 20), VIX Futures quickly turn into Backwardation, as most traders expect that it will settle down in the next 30 days or more. The steepness of the backwardation curve is usually driven by how much the VIX has spiked. The higher it goes, the more likely it is to fall further sooner, so futures predict a price much lower than the current VIX Index.

Trading Contango, Backwardation and VIX Tops and Bottoms

Now that we have a good understanding of the two types of VIX Term structures, let’s discuss where trading opportunities come from. While we only have the possibility to buy or sell VIX Futures, there are actually four distinct types of trades that arise from the behavior of the VIX and the VIX Term Structure. As our trading strategy evolved from options to VIX Futures, we began experimenting with all four of these key strategies.

Trade 1: Sell VIX Futures in Contango

We know that the majority of the time, the market stays in an uptrend or experiences small down moves that don’t significantly affect the VIX. We also know that, during those times, VIX futures are higher than the current VIX Index. We can then anticipate that, most of the time, the market will continue its overall uptrend and the VIX will remain relatively unchanged, so that at expiration the VIX Future will decline in price.

This simple trade which involves simply always shorting the soonest expiring VIX Futures is actually long term profitable on its own, as evidenced by the CBOE SHORTVOL Index, which simulates the strategy that continuously shorts a mix of 1 month and 2 month VIX Futures.

While this simplistic strategy is profitable long term, we can see that there are times where it quickly loses a lot of value, usually at big market downturns.

As discussed above, those market bottoms usually turn the futures into Backwardation. Therefore, if we sell futures when they are in Contango, we can drastically reduce those large drawdowns by closing those positions when the futures turn to Backwardation. In fact, we can even go the opposite direction….

Trade 2: Buy VIX Futures in Backwardation

The opposite of the short volatility trade exhibited above is buying VIX Futures when they are in backwardation. This anticipates that the futures will increase in price as they get closer to expiration, as long as the VIX Index itself remains elevated. This trade also works effectively, but not on a continuous basis. This is illustrated by the CBOE LONGVOL Index, which is just the opposite of SHORTVOL and constantly buys 1 month and 2 month VIX Futures.

To execute a long volatility trade requires more precision, but if we stick with the concept of only buying VIX Futures while in Backwardation, we have a much better chance of profiting during those short times and avoiding the rest of the market where buying VIX Futures would cause losses.

You can see from the chart above that after 2012 the LONGVOL Index appears to zero out. However, that is simply due to the constant losses it sustains over the extended bull markets. If we zoom into the area that we know experienced market downturns and backwardation, such as 2020, we can clearly see holding VIX Futures during those times would have been profitable, with a return as high as 300% for example in March of 2020

Holding VIX Futures continuously through any period of backwardation is still not as effective as Trade 1. This is because the VIX index peaks and futures can fall even while staying in backwardation. In fact, in the chart above, VIX Futures stayed in Backwardation until early May 2020, but we can see that the LONGVOL Index had already declined substantially from its peak by then.

This brings us to the next trade….

Trade 3: Sell VIX Futures at or near peaks in the VIX

Knowing that the VIX routinely peaks and then falls in value (VIX Mean Reversion), we can also surmise that “picking the top” would be a good strategy. One important consideration for this is that the VIX Mean Reversion and VIX Futures Backwardation are two countercurrents that work opposite each other.

We have seen that VIX Futures can fall in price when the VIX falls while still staying in backwardation, but the longer they stay in backwardation, the more likely they are to rise in price towards the value of the VIX. To illustrate this, let’s look at the March 2020 VIX Futures again in more detail.

We can see here that on March 26th, the VIX Futures were already in Backwardation, and buying them would have been profitable through March 27th, when the VIX and VIX Futures continued to increase as backwardation pushed up the price of the future close towards the VIX. However, over the next few days ending in April 6th, the VIX fell and the futures followed, dropping from around $53 to $42. Nevertheless, we know they stayed in Backwardation until early May 2020.

In this case, to make a profitable trade, it would be important to distinguish between a period of Backwardation where futures continue to increase towards the VIX, and the peak of the VIX (March 27th), where we should exit our long VIX Futures position and could have sold futures.

Trade 4: Buy VIX Futures at or near bottoms in the VIX

We can also find an opposite trade to the previous one that could generate profits at the other, low VIX, extreme. Even when futures are in Contango, the VIX will sometimes bottom out and then start a climb. Just like Backwardation, this creates countercurrent between VIX Futures Contango and the VIX itself moving up.

Simply put, the VIX futures slowly decline in price towards a lower VIX, but when the VIX rises sharply they will rise also, even if they stay in Contango.

Remember the historical chart of LONGVOL? A great opportunity to have bought futures would have been around February 18, 2020. Let’s look at the VIX Futures term structure on that date.

It is clear that the futures on that day were in Contango. Therefore, it is also important to distinguish between a continuous low VIX with VIX Futures in Contango, where we would use Trade 1, vs a bottoming VIX that precedes a sharp rise in VIX Futures (while they could still stay in Contango), where we would need to employ Trade 4.

Putting it all Together

Now that we understand the four possible VIX Futures trading strategies, we can start to put it all together into a complete trading system. In our next article, we will talk about how to prioritize the strategies and how to start determining entry and exits points more specifically. Stay tuned!

*** As always, we make it very clear that this is not investment advice, none of us are allowed to provide investment advice, this is research work product only and any trading decisions should be made on your own based on your own research and trade ideas **********